Unique Estate Planning Methods to Secure a Lifetime of Income, Save Taxes, & Benefit the Community

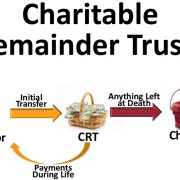

Most people planning for their retirement have a misconception that charitable giving is only for the wealthy. However, there are several estate planning tools that can benefit your favorite charity while also earning you steady stream of income. One of these tools is known as a charitable trust remainder, or “CRT.” A CRT lets you convert a highly appreciated asset like stock or real estate into a lifetime of income. It reduces your income taxes now and may also reduce your estate taxes when you die. When the assets are sold, creators of the CRT escape the ever-daunting capital gains tax. But best of all, a charitable remainder trust allows you help one or more of your favorite charities.

How does a CRT work?

Creators of a charitable remainder trust transfer an appreciated asset into an irrevocable trust. It’s important to have assets that appreciate in value in order for a CRT to work effectively. Assets that have little or no appreciation may be better off going into a charitable lead trust or charitable remainder annuity trust. In any event, when you transfer an appreciating asset into the charitable remainder trust, it removes the asset from your estate. Thus, no estate taxes will be due on it when you die. Most importantly, you also receive an immediate charitable income tax deduction.

After the trust is created, the Trustee sells the asset at full market value. Again, after the sale you will not pay capital gains tax. The money is then reinvested and the proceeds from the reinvestment go to you for the rest of your life. When you die, the remaining trust assets go to the charity(ies) you have chosen. Hence the name charitable remainder trust.

Cleveland, Ohio estate planning attorney

Example Using a Charitable Remainder Trust

Let’s say for example that Gail Giver (age 63) purchased some stock for $100,000. It is now worth $500,000. She would like to sell it and generate some retirement income. If she transfers the stock to a CRT, Gail can take an immediate charitable income tax deduction of $90,357. Because she is in a 35% tax bracket, this will reduce their current federal income taxes by $31,625.

The trust is exempt from capital gains tax so when the trustee sells the stock for the full $500,000, all of the money is available for reinvestment. Assume that the assets will accumulate 5% of annual growth and Gail is expected to live for another 26 years. Using this information, that produces $25,000 in annual income which, before taxes, will total $650,000 over Gail’s lifetime. And because the assets are in an irrevocable trust, they are protected from creditors.

Example Not Using Charitable Remainder Trust

What would happen if Gail sold the assets and reinvested them herself? If Gail sells the same $500,000 in stock, she would have a gain of $400,000 (current value less cost) and would have to pay $60,000 in federal capital gains tax (15% of $400,000). That would leave her with $440,000.

If she re-invested and earned a 5% return, that produces $22,000 in annual income. Using the same life expectancy and 5% annual income as mentioned before, this would give her a total lifetime income (before taxes) of $572,000. However, because Gail Giver still owns the assets in her name, there is no protection from creditors. Looking back, without the use of a CRT, she loses $78,000 in income than if she had created a charitable remainder trust.

Comparison of Income after Sale

Without CRT With CRT

Current Value of Stock $ 500,000 $ 500,000

Capital Gains Tax* – 60,000 0

Balance To Re-Invest $ 440,000 $ 500,000

5% Annual Income $ 22,000 $ 25,000

Total Lifetime Income $ 572,000 $ 650,000

Tax Deduction Benefit** $ 0 $ 31,625

*15% federal capital gains tax only.

(State capital gains tax may also apply.)

**$90,357 charitable income tax deduction times 35% income tax rate.

Are there other options? Of course! Another charitable estate planning tool is called the charitable lead trust, or CLT. A CLT is the reverse of a CRT. This revocable trust provides income to a charity for a set number of years, after which the remainder passes to the donor’s heirs or beneficiaries. The CLT is a good choice for those who don’t need a lifetime of income from certain assets. The trust is often structured to get an income tax deduction equal to the fair market value of the property transferred, with the remaining interest valued at zero to eliminate a taxable gift. Contact an estate planning attorney to learn more about charitable lead trusts.

Finally there is also a trust called the pooled income fund (PIF). Pooled income funds are trusts maintained by public charities. The trust is set up by donors who contribute to the fund. Just like a CRT, the donor receives income during his or her lifetime. After the donor’s death, control over the funds goes to the charity. The biggest benefit to a PIF is that contributions qualify for charitable income deductions as well as gift and estate tax deductions. Talk with an estate planning attorney to learn more.

As you can see, there are a number of different ways to give to your favorite charity while also planning for a secure retirement. This blog is meant for information purposes only and should not be construed as legal advice. Contact an estate planning attorney at Baron Law, LLC for a free consultation. Baron Law, LLC is your Cleveland, Ohio estate planning attorney. Contact Cleveland, Ohio attorney Dan Baron today at 216-573-3723